This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’m capitalizing the first letter of each word because the pervasiveness of digital transformation has all the feel of BigData a few years ago and Reeingineering in the 1990’s. It is having most impact, and will likely continue to do so, in traditional industries such as retail banking. Let’s begin there. Brand Equity.

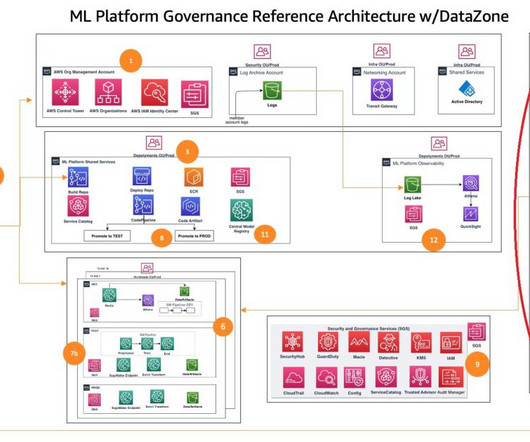

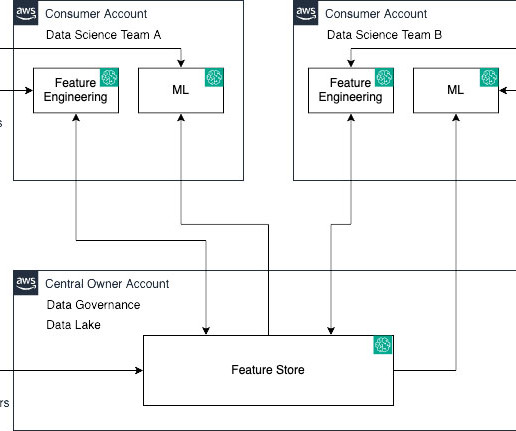

It enables different business units within an organization to create, share, and govern their own data assets, promoting self-service analytics and reducing the time required to convert data experiments into production-ready applications. The following diagram gives a high-level illustration of the use case.

The mission of Rich Data Co (RDC) is to broaden access to sustainable credit globally. Its software-as-a-service (SaaS) solution empowers leading banks and lenders with deep customer insights and AI-driven decision-making capabilities. This post is co-written with Gordon Campbell, Charles Guan, and Hendra Suryanto from RDC.

Today, banks face stiff competition from leading privatization-based technology companies. However, banks can also offer personal experiences. . Banks can use Smart IVR to provide personalized experiences to registered customers upon request. Predictive Analytics will help businesses to stay ahead and provide high-touch CX.

By now, the importance of delivering a superb customer experience in banking is crystal clear. Keeping up with the latest trends can help you understand the impact that these tendencies have on your banking customer experience. Let’s take a look at the trends that will shape the customer journey in banking in 2023 and beyond.

Similar to how a customer service team maintains a bank of carefully crafted answers to frequently asked questions (FAQs), our solution first checks if a users question matches curated and verified responses before letting the LLM generate a new answer.

In this digital age, the banks and financial institutions need to be digitally transformed to deliver a consistent customer experience in banking whether it is online or retail. Banks functioning digitally have witnessed reduced costs and streamlined processes. What is customer experience (CX) in Banking? .

Bigdata, analytics, AI and IoT continue to be hot topics, and in this 2-part blog I argue that customer data is the new marketing battleground , and that analytics are the new weapons guidance systems. Nedbank – I have walked the customer centricity journey with this great bank for over a decade.

Text dataanalytics : Call center is something of a misnomer as consumers now interact with companies via social media, email, messaging apps, and more. Text analytics programs can evaluate all those forms of communication, looking for themes and potential issues. The Process of Using BigData. Get Started Now.

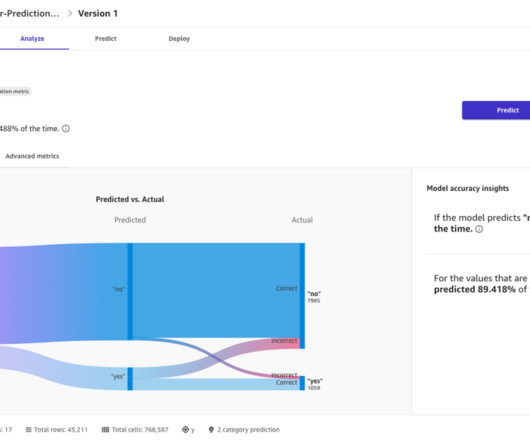

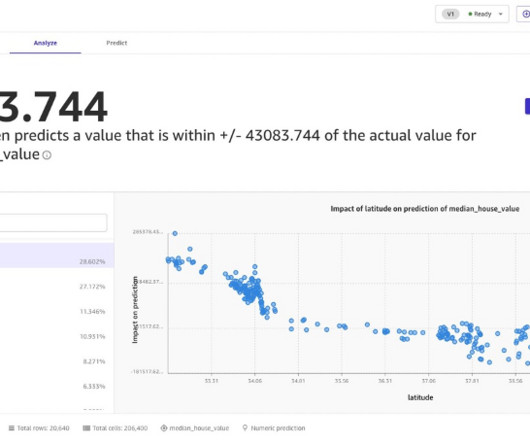

The data scientist discovers and subscribes to data and ML resources, accesses the data from SageMaker Canvas, prepares the data, performs feature engineering, builds an ML model, and exports the model back to the Amazon DataZone catalog. On the Asset catalog tab, search for and choose the data asset Bank.

In fact, the pace of change is only accelerating affecting nearly every facet of our lives, from how we bank, shop and socialize to how we respond to a pandemic. Technology is also creating new opportunities for contact centers to not only better serve customers but also gain deep insights through BigData.

Soft Data is Perfectly OK. Robust analytics platforms aren’t going anywhere. We’re now taming bigdata into impressive insights. So it’s become almost cliche to hear how a bank wants to be the “Uber” of banking or a dentist wants to offer service “like Amazon.”

At a time when credit card and bank customers in Canada are using financial institution mobile apps and websites more than ever, overall satisfaction with those digital experiences is in decline. According to a series of recent studies of bank and credit card mobile app and online users conducted in Canada, released today by J.D.

Organizations are similarly challenged by the overflow of BigData from transactions, social media, records, interactions, documents, and sensors. But the ability to correlate and link all of this data, and derive meaningful insights, can offer a great opportunity.

In todays customer-first world, monitoring and improving call center performance through analytics is no longer a luxuryits a necessity. Utilizing call center analytics software is crucial for improving operational efficiency and enhancing customer experience. What Are Call Center Analytics?

Machine learning (ML) can help companies make better business decisions through advanced analytics. His knowledge ranges from application architecture to bigdata, analytics, and machine learning. He enjoys listening to music while resting, experiencing the outdoors, and spending time with his loved ones.

The financial services industry (FSI) is no exception to this, and is a well-established producer and consumer of data and analytics. These activities cover disparate fields such as basic data processing, analytics, and machine learning (ML). The union of advances in hardware and ML has led us to the current day.

Retail banking customers who are fully engaged bring 37% more annual revenue to their primary bank than actively disengaged customers. According to this customer engagement statistic, correct engagement strategies in the retail banking sector can also result in an increase in annual revenue. Source: Gallup ) Tweet this.

RFPs for chatbots have arisen in verticals as diverse as banking, government, healthcare, and retail. In 2018, we should see much better integration with customer data and analytics, bringing customer history, behavioral patterns, and bigdata into chatbot interactions.

One challenge organizations have today is the lack of data to validate bold moves, like strategic decisions to change policies, procedures and products. Journey analytics combines bigdata technology, advanced analytics, and functional expertise to help companies perfect their customer journeys. 1- Gather the data.

When we think about the necessity of security, banking is an industry that immediately comes to mind. For banks, investing in security is simply a part of day-to-day business. Millennium bcp, Portugal’s largest bank,is an excellent example of how an enterprise can enhance its security while also achieving enormous savings.

Companies use advanced technologies like AI, machine learning, and bigdata to anticipate customer needs, optimize operations, and deliver customized experiences. Creating robust data governance frameworks and employing tools like machine learning, businesses tend derive actionable insights to achieve a competitive edge.

Furthermore, the integration of digital technologies, including artificial intelligence, blockchain, and bigdata, augments these ESG capabilities. The dynamic nature of ESG metrics and their multifaceted relationship with CFP necessitates a detailed and layered analytical approach.

Digital Transformation might not be so relevant now if not for the major technological changes of the last decade: bigdata and analytics, social (consumer and enterprise), mobility, and the cloud. When blockchain is mentioned, most people think of banks. Blockchain. Platforms, not Tools.

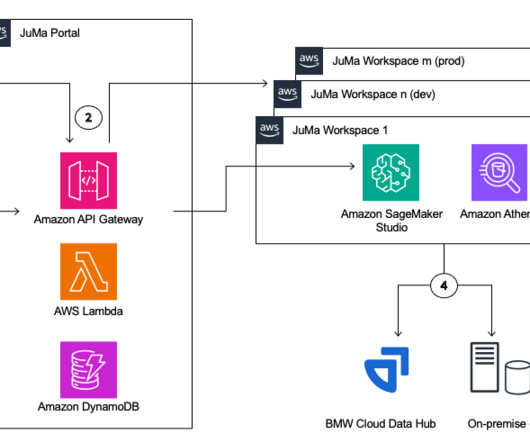

This offering enables BMW ML engineers to perform code-centric dataanalytics and ML, increases developer productivity by providing self-service capability and infrastructure automation, and tightly integrates with BMW’s centralized IT tooling landscape. Joaquin Rinaudo is a Principal Security Architect at AWS ProServe.

Whether via social media, websites, or online communities, companies can gather a massive amount of digital data on their customers. Companies can then use AI-driven predictive analytics tools to determine customer patterns or trends in order to better target their marketing offers, and enhance their relationship with customers.

Whether via social media, websites, or online communities, companies can gather a massive amount of digital data on their customers. Companies can then use AI-driven predictive analytics tools to determine customer patterns or trends in order to better target their marketing offers, and enhance their relationship with customers.

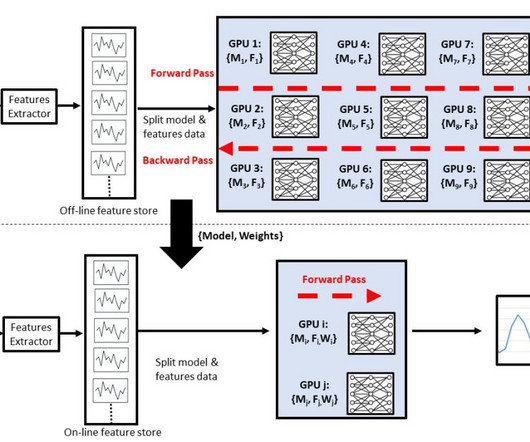

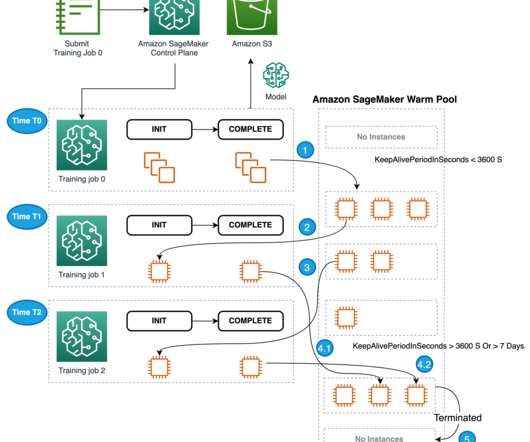

Workflow significantly impacts productivity, and data scientists prefer Jupyter Notebooks for their faster iteration cycles. This preference is closely tied to the “ Roman Census approach ” central to BigData. When a data scientist prepares gigabytes of data or a large model, it might take seconds or minutes.

For example, the analytics team may curate features like customer profile, transaction history, and product catalogs in a central management account. Their aim is to feed data into a centralized feature store, establishing it as the undisputed reference point. The hurdle they often face is redundancy.

Plus, businesses in banking, financial services, and others are busy wrapping up the year and prepping for the next. For instance, leading BPOs now employ advanced AI-driven analytics to personalize customer interactions, a concept barely conceivable three years ago. This time of year is crucial for many industries.

His knowledge ranges from application architecture to bigdata, analytics, and machine learning. Prior to joining AWS, Hariharan was a product architect, core banking implementation specialist, and developer, and worked with BFSI organizations for over 11 years. Hariharan Suresh is a Senior Solutions Architect at AWS.

In a world where customers can bank, shop, and book travel with a few clicks, they expect the same level of convenience from their financial providers. These companies are able to provide a smoother customer experience by leveraging cutting-edge technologies such as cloud-based banking, mobile apps, and BigDataanalytics.

Picture bank tellers that can identify customers (or criminals) as soon as they walk through the door via facial recognition. A retailer may be focused on detecting the proximity of a customer in order to push relevant promotions based on bigdataanalytics.

In fact, the pace of change is only accelerating affecting nearly every facet of our lives, from how we bank, shop and socialize to how we respond to a pandemic. Technology is also creating new opportunities for contact centers to not only better serve customers but also gain deep insights through BigData.

Through bigdataanalytics, companies can create a personalized journey for each of their customers. Drift reports that chatbots are the fastest-growing brand communication channel, while CNBC notes that they are predicted to handle up to 90% of all banking and healthcare queries made in 2022.

This next-generation CX is supported by several advanced technologies—bigdataanalytics, omnichannel, automation—however, these investments are all aimed at driving one thing: contextualization. But what exactly does the CX consist of, especially in today’s new world of digital business innovation?

Front-end sales – train the latest AI tools to answer the most common questions quickly then maximise their ability to use critical customer data to offer personalised recommendations on policies and pricing. Also remember that AI tools thrive on good data so build a bank of reliable data that is up-to-date and above all, relevant.

Today, we have the ability to use AI and bigdataanalytics to listen and understand at scale—effectively delivering the benefit that a team of business analysts would, but without the cost or time required to do the work manually. Technology has come a long way since 2013 when CEB published the book.

Royal Bank of Scotland manages 17 million customers but managed to raise its Net Promotor Score by 18 points unanimously after deploying AI while US telecommunications giant Sprint achieved a 14% increase in customer retention in just six months, simultaneously overcoming an industry-high in turnover rates.

This enables the broader sharing of resources across the bank enterprise, whether they are in a contact center or another location. Gary Ambrosino, CEO of TimeTrade goes on to say, “In-branch service has been suffering, and banks are losing customers as a result. What Do The Executives Have to Say?

CEM 7th Annual Customer Experience Management Banking Summit April 10 – 12, Vienna. Monetising BigData in Telecoms World Summit 2018 April 23 – 24, Singapore. This year’s Summit will host speakers from the world’s leading companies. HDI 2018 – Conference and Expo April 10 – 13, Las Vegas, NV.

In a recent ETCIO.com article , Firstsource’s Aparajita Gupta, senior vice president, digital support and analytics, describes how using Verint Speech and Text Analytics helped the India-based business process outsourcer analyze huge volumes of data and—importantly for its customers—find root causes to a variety of challenges.

Nowadays, there are so many options to make payments like bank transfer, third-party payment gateways e.g. Paypal, digital money etc. This data can be used for future, and even for generating insights via the implementation of BigDataanalytics. Processing of payments.

Reacting after the fact to an unforeseen security event used to be the only option for bank officials. At an ATM, branch, corporate campus or even an online banking website, the minute a security incident begins, officials have no time to waste.

We organize all of the trending information in your field so you don't have to. Join 34,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content