This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’m capitalizing the first letter of each word because the pervasiveness of digital transformation has all the feel of BigData a few years ago and Reeingineering in the 1990’s. It is having most impact, and will likely continue to do so, in traditional industries such as retail banking. Let’s begin there.

As we move towards bigdata and artificial intelligence, chatbots seem to be leading the way towards a more automated future. In 2010, the boys over at Apple released Siri that astounded the world because for the first time you had a super-commercial chatbot/personal assistant that was so easy to have the mass market adapt to.

By now, the importance of delivering a superb customer experience in banking is crystal clear. Keeping up with the latest trends can help you understand the impact that these tendencies have on your banking customer experience. Let’s take a look at the trends that will shape the customer journey in banking in 2023 and beyond.

The UK CSI has companies routinely appearing in the top 10, like Amazon, John Lewis (which is like Nordstrom), Next (a retailer), the bank First Direct and Nationwide. They successfully blend virtual and personal experiences and knowing when to deploy which in certain situations. . The Fly in the Ointment Regarding Personal Context.

Here are three great companies, Amazon, Southwest Airlines and TD Bank (I wouldn’t have guessed this last one), that are relentless when it comes to being customer focused. Use Emojis and Other Tips to Make Customer Service More Personal by Dianna Labrien. All are great concepts that are appropriate for just about any company.

Personally, I’m not so sure. At the front of the store, where you’d usually find checkout lines, there is a bank of electronic turnstiles. Be Warned: You Can’t Rely on BigData! At least that’s what some people think. To listen in, please click here . It’s Essential: Understand Your Customer’s Habits!

In this digital age, the banks and financial institutions need to be digitally transformed to deliver a consistent customer experience in banking whether it is online or retail. Banks functioning digitally have witnessed reduced costs and streamlined processes. What is customer experience (CX) in Banking? .

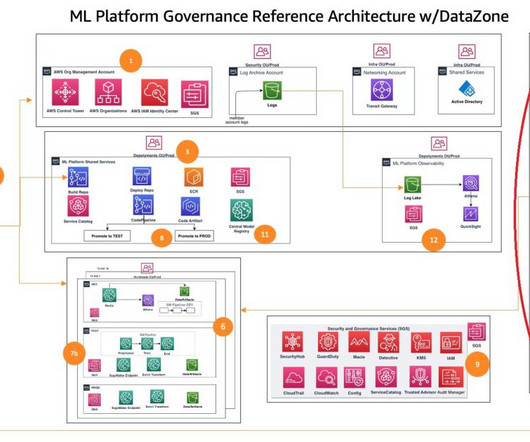

By taking advantage of the data governance capabilities of Amazon DataZone, financial institutions like banks can securely access and use their comprehensive customer datasets to design and implement targeted marketing campaigns tailored to individual customer needs and preferences.

This means instead of having the “customer experience person,” they have full teams of specialized people. Soft Data is Perfectly OK. We’re now taming bigdata into impressive insights. It will take continued dedication and diligence, but you are just the person to do it. So roll up your sleeves.

Sources like CNBC and The Telegraph predict that the retail bank branch will die within the next decade. In fact, the market is heading towards bank branch innovation unlike anything we’ve ever seen. Traditional vendors must now compete alongside newer digital-only banks like Ally in the U.S., In Italy, banks like CheBanca!

Personalized Customer Engagement. Extensive personalization using the next best action increases average revenue per user by 166 percent. By providing a personalized support experience, it becomes a hassle-free task for any business not only to increase customer engagement but revenues too. Personalized Customer Engagement.

Of everything a business-to-business (B2B) company must be great at in order to grow, delivering personalized customer support at scale needs to be a priority. Making customer support personalized, then continually improving upon the experience is what truly shows your customers that they are a top priority for you. You Have Data.

In fact, the pace of change is only accelerating affecting nearly every facet of our lives, from how we bank, shop and socialize to how we respond to a pandemic. The consumer experience is becoming easier, faster and more personable. This helps agents provide faster, more personalized services that meet customer expectations.

In part 1, we described the data capture and document classification stages, where we categorized and tagged documents such as bank statements, invoices, and receipt documents. We run the get_entities() method on the bank document and obtain the entity list in the results. Then we train a custom entity recognition model.

Nearly all of us have felt the impact of digital transformation from the interactions in our day-to-day personal or professional lives — from interactive teller machines (ITMs) appearing at local community bank branches to virtual visit technology being deployed by doctors’ offices around the country. The Potential Risk.

bank cards) or personal. In the last couple of years there has been a recurring theme on media press sites covering technology, of companies compromising the security and belittling the value of their customers information – whether it be dangerous (i.e.

An agent could be a bank teller, a nurse, or a computer technician. They just happen to be doing their job while interacting remotely, rather than in person. Well, it’s meaningless to talk about anything “replacing a call center agent” because that’s not a specific job (like, say, a shoemaker). Self-Service Substitution.

RFPs for chatbots have arisen in verticals as diverse as banking, government, healthcare, and retail. In 2018, we should see much better integration with customer data and analytics, bringing customer history, behavioral patterns, and bigdata into chatbot interactions.

The bigbanks will be left tightening up their credit belts, meaning customers will turn to their local credit unions for loans. Some trends, like video banking, will transform into a credit union mainstay as it lets members talk face-to-face to an agent, while credit unions can centralize their workforce.

Digital Transformation might not be so relevant now if not for the major technological changes of the last decade: bigdata and analytics, social (consumer and enterprise), mobility, and the cloud. When blockchain is mentioned, most people think of banks. Blockchain. Platforms, not Tools.

Plus, businesses in banking, financial services, and others are busy wrapping up the year and prepping for the next. For instance, leading BPOs now employ advanced AI-driven analytics to personalize customer interactions, a concept barely conceivable three years ago. This time of year is crucial for many industries.

Deliver personalized customer experiences. An important way financial services companies can improve the customer experience is by personalizing the service they provide. In a world where customers can bank, shop, and book travel with a few clicks, they expect the same level of convenience from their financial providers.

The bigbanks will be left tightening up their credit belts, meaning customers will turn to their local credit unions for loans. Some trends, like video banking, will transform into a credit union mainstay as it lets members talk face-to-face to an agent, while credit unions can centralize their workforce.

BigData = Big Opportunity. It’s Business AND it’s Personal First and foremost, data reigns supreme. As highlighted in the report, the past decade has seen organisations amassing vast amounts of ‘bigdata’ However, the real challenge lies in making this data accessible and actionable.

Personalizing the Customer Experience. Through bigdata analytics, companies can create a personalized journey for each of their customers. Consumers are expecting more personalized, pertinent, and efficient support than ever before.

This next-generation CX is supported by several advanced technologies—bigdata analytics, omnichannel, automation—however, these investments are all aimed at driving one thing: contextualization. But what exactly does the CX consist of, especially in today’s new world of digital business innovation?

But modern analytics goes beyond basic metricsit leverages technologies like call center data science, machine learning models, and bigdata to provide deeper insights. Predictive Analytics: Uses historical data to forecast future events like call volumes or customer churn.

This enables the broader sharing of resources across the bank enterprise, whether they are in a contact center or another location. Gary Ambrosino, CEO of TimeTrade goes on to say, “In-branch service has been suffering, and banks are losing customers as a result. What Do The Executives Have to Say?

Using bigdata analytics, machine learning and AI, Guavus subscriber intelligence products provide 360 degree insights into individual customer preferences and experiences. Braze (formerly Appboy) is a lifecycle engagement platform that delivers personalized messaging experiences that span across channels, platforms, and devices.

Using bigdata analytics, machine learning and AI, Guavus subscriber intelligence products provide 360 degree insights into individual customer preferences and experiences. Braze (formerly Appboy) is a lifecycle engagement platform that delivers personalized messaging experiences that span across channels, platforms, and devices.

Picture bank tellers that can identify customers (or criminals) as soon as they walk through the door via facial recognition. Meanwhile, a financial institution is concerned with how to guarantee account protection and secure financial transactions while providing a personalized experience for customers.

Telephone banking was one of the first self-serve interactions that most of us experienced. Business rules tied to applications, and informed by bigdata and data mining, can drive proactive interactions with or without an agent involved. . AI continues this evolution.

Due to customer-centric companies like Amazon and an increased personalization of offers, now people accept nothing less than playing the role of captain in the retail journey. Personal with an AI twist. A dedicated personal account manager is no longer an option, considering the scale of operations.

The idea of using bigdata to program software is not new. Research shows that almost 97% of mobile users are using these voice-based personal assistants that are based on AI. Web3 is a decentralized network of devices where data is stored autonomously that is not controlled by any person or company.

In fact, the pace of change is only accelerating affecting nearly every facet of our lives, from how we bank, shop and socialize to how we respond to a pandemic. The consumer experience is becoming easier, faster and more personable. This helps agents provide faster, more personalized services that meet customer expectations.

Ecommerce doesn’t have much of the friction of in-person shopping, but it’s also removed much of the friction for credit card fraud as well, enabling fraudsters to advantage of the limited identification mechanisms available for online purchases. BigData to the rescue: Use your data of previous transactions.

Such issues include collecting personal patient data without consent in healthcare or over-reliance on machine-led decisions without disclosure in banking and insurance. Follow this formula to build consumer trust and confidence.

Contact Center AI can enhance agent performance, provide a more personalized customer support experience, and make customers happier. One example is when a banking customer wants to deactivate their credit card if they suspect it’s stolen. What Can Contact Center AI Do?

With suites there is the opportunity to know your customers better, via shared data, shared knowledge across lines of business for personalized and relevant offers, products and services. In fact, 67% of a decision on what to buy in B2B sales is completed before the customer even talks to a sales person.

and when the visitor selects “Sales,” the bot might direct that person to a page explaining how a solution caters to sales teams. A few examples: A banking app might use rules-based chatbots to answer questions like “How do I find my routing number?” Then, it runs that data against behavioral data, usage history, etc.,

But over time, I moved into banking technology, I rose up the ranks and I ended up running all of the trading technology for a big French bank. And then after that job, I ran European technology for an American bank. I don’t want to get up early and go to the bank every morning.

a personal assistant for those with busy calendars, Royal Bank of Scotland’s Luvo in the financial services industry, and beyond. What if a customer has multiple orders, is travelling with a companion that paid for them both, or is using their company account and not their personal one? This should come as no surprise.

You open your favorite travel app or website, enter your destination, and instantly get personalized recommendations for flights, hotels, and activities. Companies use advanced technologies like AI, machine learning, and bigdata to anticipate customer needs, optimize operations, and deliver customized experiences.

Gerry explains some interesting back stories to the approach of Four Seasons, amidst other brands, as well as his personal experience with one Holiday Inn. From cloud computing solutions and use of bigdata to organisational alignment and Bring Your Own Attitude. Here is a link to see the GoodReads preview for this book.

We organize all of the trending information in your field so you don't have to. Join 34,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content